credit scoring

If you're struggling with debt, you're not alone. According to the Institute of International Finance (IIF), global debt reached a record high of $296 trillion by the end of June 2021, which was approximately 350% of global GDP. This total includes household, corporate, and government debt, highlighting the extensive scale of debt worldwide.

Millions of individuals and households around the world face the weight of unpaid bills, mounting interest, and financial uncertainty. But here’s the good news: there are solutions. They come in the form of effective debt management tactics, often guided by professional debt managers who are trained to help you navigate these challenges with clarity and purpose.

In this guide, we’ll break down the top debt management strategies, explain what debt managers do, and help you understand how to tackle your financial situation step-by-step.

A Debt Management Plan (DMP) is a formal agreement between you and your creditors, facilitated by a credit counselor or a debt management expert. It’s designed to help you repay your unsecured debts, like credit card bills, personal loans, or medical bills, in a more manageable way.

Once you enter a DMP, you’ll make a single monthly payment to a credit counseling agency or debt manager, who will then distribute the funds to your creditors. This reduces the complexity of managing multiple payments and helps you stay organized, all while allowing you to focus on paying off your debt.

Debt management is especially beneficial for managing unsecured debts, which are debts not tied to any collateral. This includes:

High-interest credit card balances are one of the most common financial burdens. Debt managers can help you consolidate these debts, potentially lowering interest rates and creating a realistic repayment plan.

While personal loans can be a great option when you need immediate funds, they can become overwhelming if not managed properly. Debt management strategies can help you restructure these loans to make repayment more manageable.

By focusing on these types of debts, debt management makes it easier to regain control, reduce stress, and make consistent progress toward eliminating your financial burdens.

Knowing what debt management is only scratches the surface. Next, it’s essential to understand why it matters and how a tailored strategy can make or break your path to financial recovery.

When it comes to tackling debt, one-size-fits-all solutions simply don’t work. A personalized debt management plan considers your specific income, expenses, and the types of debts you have.

Debt management isn't just about getting out of debt, it's about doing it in a way that works best for you. Your income, living expenses, and the type of debts you have all affect the best plan for you.

Example: if you're living paycheck to paycheck, a debt manager might suggest a plan that focuses on lowering your monthly payments and reducing interest rates. But if you can afford to pay more each month, they might recommend a faster plan to pay off your debts more quickly.

A plan made just for you helps you pay off your debts while still being able to live comfortably. It ensures you’re not stretching your budget too thin or making sacrifices that could hurt your mental health or your family life.

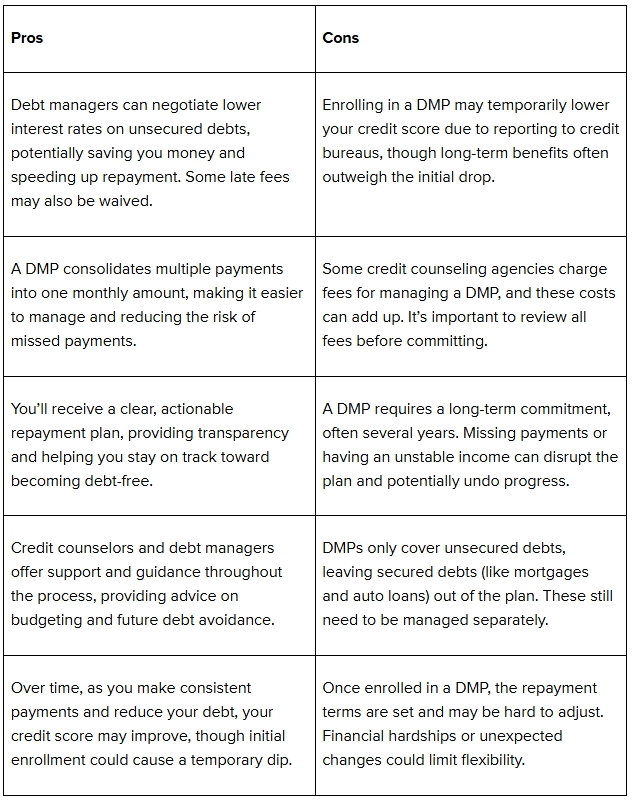

DMP can secure lower interest rates and eliminate late fees on your debts. This can reduce the total amount of money you pay over time and help you pay off your debt faster.

With a DMP, you’ll make one monthly payment instead of managing several different due dates and payment amounts. This reduces the risk of missing payments, which can negatively impact your credit score.

A well-structured DMP gives you a clear timeline for becoming debt-free. While it may take several years to pay off your debts, having a concrete plan in place can provide peace of mind and help you stay focused on your goal.

While a DMP itself doesn’t erase your debt or improve your credit score immediately, sticking to the repayment plan and making timely payments can gradually improve your credit score over time. This is especially true if the debt manager is able to have late fees or interest charges waived.

By matching the debt management plan with your specific financial situation, you can often reduce interest payments and shorten the repayment timeline. This means you can become debt-free faster than you might have anticipated, saving you money in the long run.

Once you understand how important it is to have a personalized plan, the next step is figuring out the best way to manage your debt. Let’s look at some practical methods that can help you take control.

When you're faced with mounting debt, taking control of your finances is the first step toward regaining peace of mind. While professional debt managers can offer tailored advice and assistance, there are also self-directed strategies you can use to tackle debt on your own.

Two of the most popular debt repayment methods are the debt snowball and debt avalanche techniques. Both methods focus on organizing your debts in a way that allows you to make consistent progress.

With this technique, you focus on paying off your smallest debt first, regardless of interest rate, while making minimum payments on your larger debts. Once the smallest debt is paid off, you move on to the next smallest, and so on, gradually paying off your debts in order of size.

Example:

Here, you would focus on paying off the $500 credit card first. Once it's paid off, you roll that payment amount (along with your previous minimum payments) into paying off the $2,000 personal loan. Finally, you would tackle the $5,000 auto loan.

The key benefit of this approach is the emotional boost you get from quickly eliminating debts, which keeps you motivated to continue.

The debt avalanche method, on the other hand, focuses on paying off your highest-interest debts first. After making the minimum payments on all of your debts, any extra money goes toward the debt with the highest interest rate. Once that’s paid off, you move on to the next highest interest rate, and so on.

Example:

In this case, you would focus on paying off the $2,000 personal loan with 10% interest first since it has the highest interest rate. After eliminating that, you would move on to the $5,000 auto loan with 4% interest, and lastly, tackle the $500 credit card balance.

The benefit of the avalanche method is that it saves you money on interest over time since you prioritize the debts that cost you the most.

Managing debt on your own requires both planning and organization. Thankfully, there are numerous tools available that can make this process easier and more efficient.

Budget calculators show you where you can cut back on spending to free up more money for debt repayment. Budget calculators break down your expenses into categories, allowing you to see exactly where your money is going. By tracking your spending, you can identify areas where you can save, making it easier to allocate more money to pay down your debt.

Repayment apps are designed to make debt management easier by automating your payments and tracking your progress. These apps can help you stay organized by setting up reminders, suggesting payment amounts, and even sending payments directly to creditors. Some apps even allow you to track multiple debts simultaneously.

Credit counselors are trained professionals who can assist with debt management by negotiating with creditors to lower interest rates, reduce monthly payments, or even settle debts for a lower amount. Credit counselors provide a range of services to help you manage your debt, including:

With your options and using the right resources, you can make meaningful progress toward becoming debt-free and regaining financial control.

If you’re considering structured help, a DMP might be the right fit. Here's a closer look at how DMPs actually work.

A DMP is typically organized and managed by a debt manager or a credit counseling agency. By enrolling in a DMP, you can gain control over your debt and make consistent progress toward becoming debt-free.

The first step in a DMP is a comprehensive assessment of your financial situation. It involves evaluating your income, expenses, and debts to determine the best course of action. You’ll also know your financial goals and how much you can realistically afford to pay each month toward your debts.

DMP allows debt managers to work on your behalf to negotiate with creditors. The goal is to reduce your interest rates, waive late fees, and possibly extend your repayment terms. This can lower your monthly payments and make your debts more manageable.

Instead of juggling multiple creditors and due dates, a DMP consolidates your unsecured debts into a single monthly payment. You’ll send one payment to the credit counseling agency, which will then distribute it to your creditors. This simplifies your repayment process and ensures that you don’t miss any due dates.

The DMP provides you with a clear, structured plan for paying off your debts. You set a reasonable timeframe for repayment, typically ranging from 3 to 5 years, depending on your total debt load. During this time, you’ll make regular monthly payments until your debts are fully paid off.

A significant part of a DMP is the ongoing support you’ll receive from the credit counseling agency or debt manager. They’ll monitor your progress, offer budgeting advice, and provide emotional support as you work toward debt freedom.

Pro Tip: Some credit counseling agencies charge fees for managing a DMP, although these fees are typically small. It’s important to choose a reputable agency that is transparent about any charges.

When considering a DMP, South East Client Services (SECS) can be your trusted partner in managing your receivables and debt recovery. SECS provides expert services that include negotiating with creditors, lowering interest rates, and consolidating payments, ensuring your debt repayment process is simplified and effective. With their ethical approach to collections and focus on compliance, SECS helps you regain control of your financial situation while protecting your reputation. Get SECS today.

Like any financial strategy, a DMP comes with both upsides and limitations. Let’s weigh the pros and cons to help you decide if this approach suits your financial goals.

A DMP can offer a structured way to reduce debt, but like any financial strategy, it comes with its own set of advantages and drawbacks. With both, you can decide and better prepare for what lies ahead.

While a DMP offers many advantages, it's essential to ensure that you’re ready for the commitment and fully understand how it may impact your credit score and financial flexibility.

Another key factor to consider is how debt management can affect your credit. From short-term dips to long-term growth, here’s what you need to know before making a decision.

Entering a DMP doesn’t automatically mean your credit score will improve. In fact, it may initially have a negative effect on your score. This is because creditors may report your enrollment in a DMP to credit bureaus, which can signal that you're experiencing financial difficulties. The presence of a DMP on your credit report can make it seem like you're not handling your debts as successfully as you could be.

However, the impact is often temporary. The initial dip in your credit score is typically due to the following:

While these effects are usually short-term, they do contribute to a drop in your credit score when you first enter a DMP. But don’t let this discourage you; it’s part of the process of rebuilding your financial health.

Once you’ve enrolled in a DMP and started making consistent, on-time payments, you can begin to see improvements in your credit score. Here’s how consistent, responsible behavior can improve your score over time:

Your payment history accounts for 35% of your credit score. By making regular, on-time payments through a DMP, you demonstrate to creditors that you are responsible and committed to clearing your debts. As you consistently make payments, your credit score will eventually improve.

As you pay off debts through the DMP, your total debt decreases, which improves your debt-to-income ratio. This ratio is an important factor that lenders use to assess your financial health. A lower debt-to-income ratio signals that you’re better able to manage and repay any new debt, which can lead to a higher credit score.

Reducing outstanding balances on credit cards and loans decreases your credit utilization rate, which is another important factor in your score. As you pay off debt through a DMP, your credit utilization decreases, boosting your score in the process.

Over time, creditors may begin to update their reporting to reflect your improved payment habits. This can lead to more favorable reports to the credit bureaus, which, in turn, can improve your credit score.

While it may take some time to see improvements in your credit score, consistently following your DMP can pave the way for a stronger credit history and a brighter financial future.

Improving your credit score is important, but so is understanding the potential risks. Before you commit, make sure you're aware of the challenges that can come with a Debt Management Plan.

Every financial strategy has its potential downsides, and DMPs are no exception. By knowing these risks upfront, you can know if a DMP is right for you and how to mitigate any potential issues.

A DMP typically takes 3 to 5 years to complete. While this extended timeline can help you pay off debt in a manageable way, it also requires a long-term commitment. You must remain consistent with your payments throughout the plan to successfully eliminate your debt.

While a DMP is highly effective for unsecured debts, like credit cards and personal loans, it doesn’t cover secured debts, such as mortgages, car loans, or student loans. This means that while your DMP may reduce or eliminate your unsecured debt, you’ll still need to manage secured debt on your own.

Some debt management agencies promise quick fixes and debt-elimination strategies that turn out to be fraudulent. These agencies may charge high fees for services that don’t lead to real results or even create more debt for you.

While you’re enrolled in a DMP, you may be restricted from obtaining new credit. Some creditors may block you from opening new credit lines, while others may impose higher interest rates. This can limit your ability to make major purchases, like buying a car or securing a loan for a home.

While a DMP can manage unsecured debt, the potential negative effects on your credit score, long-term commitment, lack of relief for secured debts, fees, and the risk of scams are all factors to consider.

If a DMP doesn’t seem like the right fit, don’t worry, you’ve got options. Let’s look at some effective alternatives that may better align with your financial needs and lifestyle.

Depending on your financial situation, there are other options to consider that might be a better fit for you. These alternatives can offer more flexibility, faster results, or even less impact on your credit score.

A balance transfer credit card with 0% APR transfers your high-interest credit card balances to a new card offering 0% APR for an introductory period of typically 12 to 18 months. This can give you a break from interest charges and help you pay down your debt more quickly.

How Does It Work?

Pro Tip: If you have good to excellent credit and are able to pay off your balance within the promotional period, a balance transfer credit card can be a great way to save money on interest and pay down your debt faster. However, it’s important to stay disciplined and avoid accumulating new debt on the card.

A debt consolidation loan involves taking out a loan to pay off multiple debts, leaving you with one single loan to manage. The goal is to simplify your finances by consolidating high-interest debts, such as credit card balances or personal loans, into a single payment with a potentially lower interest rate.

How It Works

Pro Tip: A debt consolidation loan is ideal if you have several high-interest debts and can qualify for a loan with a lower interest rate. It’s also a good option if you prefer having a single payment rather than juggling multiple debts. However, if you’re not confident in your ability to resist new debt or don’t qualify for favorable loan terms, this may not be the best solution for you.

Bankruptcy is often seen as a last resort, but it is an option for those facing insurmountable debt. There are two primary types of bankruptcy for individuals. Each type offers different solutions and comes with its own set of consequences.

Bankruptcy will significantly impact your credit score. A Chapter 7 bankruptcy can stay on your credit report for up to 10 years, and Chapter 13 for up to 7 years. This can make it challenging to secure new credit, obtain loans, or rent housing during that period.

Pro Tip: Bankruptcy is often best for individuals who have no realistic way of repaying their debts and are overwhelmed by financial obligations. It’s important to explore other options, like DMPs or debt consolidation loans, before resorting to bankruptcy.

While a DMP can be a great solution for managing debt, it’s not the only option available. Depending on your financial situation, alternatives like balance transfer credit cards, debt consolidation loans, or even bankruptcy may provide a better fit.

With multiple paths available, how do you decide what works best for you? This next section helps you evaluate which debt management solution fits your current situation.

If you’re considering working with debt managers, consolidating loans, or exploring bankruptcy, matching your debt management approach to your circumstances is key to long-term success.

Different strategies suit different types of debt and financial behaviors. Let’s break down who fits best with each major option:

Choosing the wrong strategy can delay progress or, worse, dig the hole deeper. That’s why working with a trustworthy debt manager or certified credit counselor can help clarify your best path forward.

Not all financial challenges require the same response. Choosing a DMP or any other debt relief solution depends on the nature and severity of your situation. Here's how to decide if a DMP is based on your specific circumstances:

Even if you haven’t missed any payments, interest charges might be eating away at your income. A DMP is suitable here because debt managers can negotiate reduced rates with creditors. You’ll maintain a solid payment record while paying less over time.

If you’ve started falling behind and creditors are calling, a DMP can help stop the calls, restructure your payments, and help you catch up. Most creditors will pause or reduce collections once you’re enrolled in an approved DMP.

Using credit cards to cover food, gas, or rent? That’s a warning sign. A DMP can help you break that cycle by consolidating your unsecured debts into a single payment, and avoid relying on credit for daily living.

Unexpected medical bills or emergency expenses can derail even a solid financial plan. If your debt is primarily unsecured and manageable through structured payments, a DMP may be your best choice. If it’s larger than your income can support, you may need to consider consolidation or legal options.

For those who want to preserve their credit as much as possible and avoid the long-term effects of bankruptcy, a DMP provides a middle ground. It won’t eliminate debt as quickly as bankruptcy might, but it also won’t damage your credit as severely.

Choosing the right debt management strategy is about aligning your solution with your financial reality. The right plan helps you regain control without creating new problems.

When it comes to managing your debt, there isn't just one right solution. If you're thinking about a Debt Management Plan (DMP), debt consolidation, or other options like balance transfer credit cards or even bankruptcy, the most important thing is to find a plan that works best for your specific financial situation.

Working with experienced debt managers can help you with your options and create a plan to reduce stress, lower interest rates, and get you back on track to financial freedom. By staying disciplined with your payments, learning about your options, and getting professional help when needed, you can take control of your debt and set yourself up for long-term success. Finding the right strategy for your situation can make a big difference.

Partnering with a trusted expert like South East Client Services (SECS) ensures you receive tailored advice, clear strategies, and ethical solutions to streamline your debt recovery. Let SECS handle your receivables with confidence and help you towards financial freedom. Get in touch today.